![The Logan Bartlett Show: Mike Volpi Predicts the Future of AI Wave [Summary + Transcript]](https://storage.ghost.io/c/18/b5/18b50ec6-aaa0-4f89-82bd-97facf43831a/content/images/size/w2000/2024/03/Podcast-Banner-The-Logan-Bartlett-Show.jpg)

Logan Bartlett sits down with Mike Volpi, General Partner at Index Ventures and the powerhouse investor behind tech giants like Confluent, Scale AI, and Sonos. They delve into Mike's investment strategies, the next wave of AI innovation, his career at Cisco, and more.

Here's a quick summary of their insightful conversation:

The Logan Bartlett Show: Top AI investor predicts how AI wave will play out—Summary powered by Fireflies.ai

Outline

- Chapter 1: Introduction and Background (00:15 - 01:19)

- Chapter 2: Conversations on Early Career at Cisco (01:20 - 01:39)

- Chapter 3: Venture Capital and Entrepreneurship (01:40 - 03:03)

- Chapter 4: Discussing Tech Industry and AI (03:04 - 09:01)

- Chapter 5: Investing in Tech and Understanding the Market (09:02 - 12:11)

- Chapter 6: Insights on Business Trends and Internet Shifts (12:12 - 14:45)

- Chapter 7: Understanding SaaS Applications (14:46 - 17:11)

- Chapter 8: Debating about Large Language Models (17:20 - 21:31)

- Chapter 9: Highlighting Aurora and Scale.ai (24:05 - 24:21)

- Chapter 10: Role as a Venture Capitalist and Decision Making (26:14 - 28:35)

- Chapter 11: Frameworks for Making Investment Decisions (28:36 - 31:02)

- Chapter 12: Lessons from Opsware and Cisco Days (31:03 - 33:55)

- Chapter 13: The Role of Adaptability in Tech (33:56 - 36:11)

- Chapter 14: Cisco's Investing Strategy and Learning about M&A (36:12 - 38:28)

- Chapter 15: Journey at Index Ventures (38:29 - 41:03)

- Chapter 16: Learning and Growing in the Venture Capital Industry (41:04 - 44:10)

- Chapter 17: Reflecting on Past Mistakes and Learning (44:11 - 48:08)

- Chapter 18: Insights on Ferrari and Luxury Brands (48:09 - 51:38)

- Chapter 19: Discussing Current Market Dynamics and Investing Trends (51:39 - 54:58)

- Chapter 20: Reflections on Board Membership and Relationships (54:59 - 58:44)

- Chapter 21: Market Leaders and Investment Choices (58:45 - 1:02:11)

- Chapter 22: Advice for Young Professionals in Tech (1:02:12 - End)

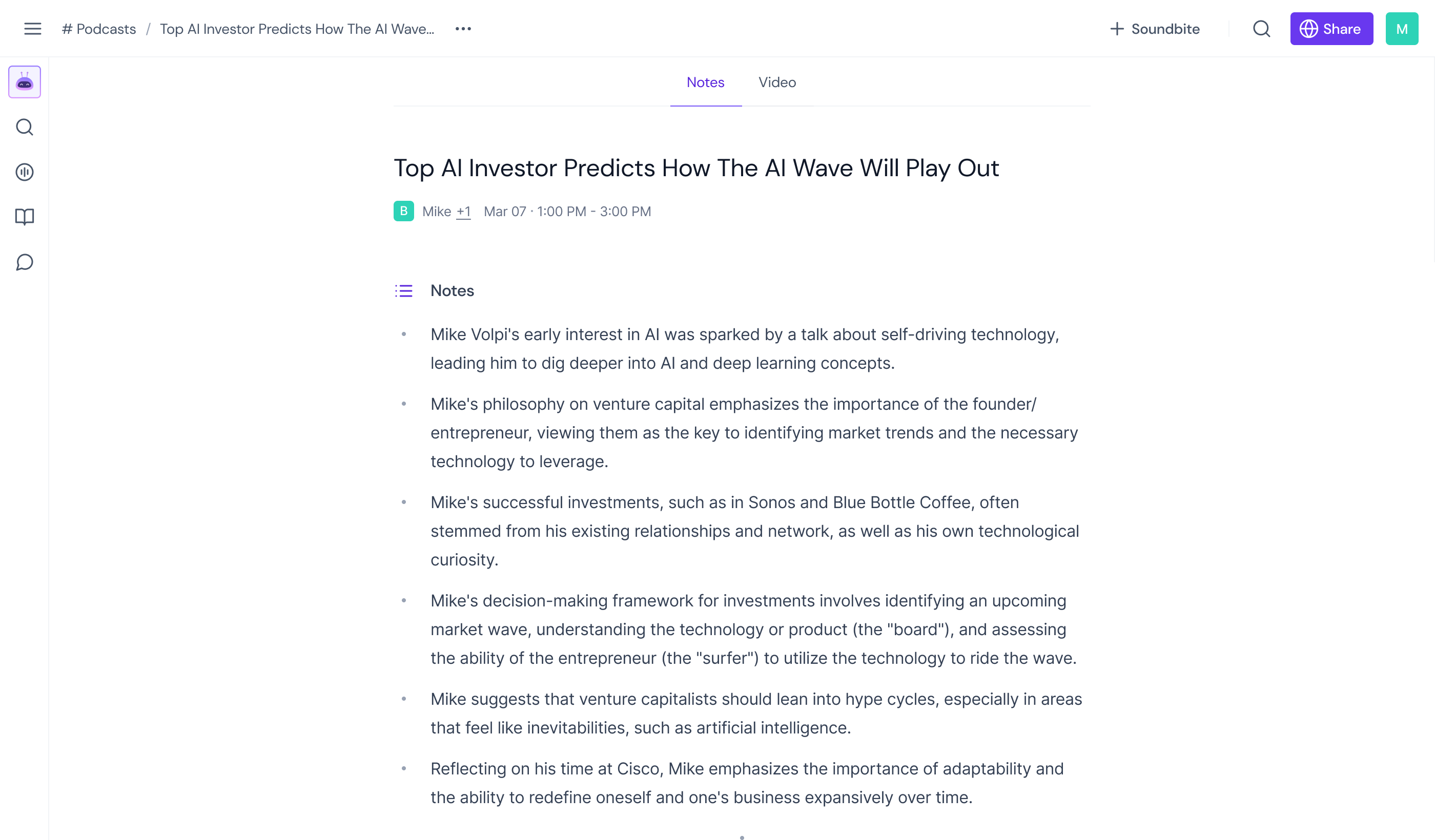

Notes

- Mike Volpi's early interest in AI was sparked by a talk about self-driving technology, leading him to dig deeper into AI and deep learning concepts.

- Mike's philosophy on venture capital emphasizes the importance of the founder/entrepreneur, viewing them as the key to identifying market trends and the necessary technology to leverage.

- Mike's successful investments, such as in Sonos and Blue Bottle Coffee, often stemmed from his existing relationships and network, as well as his own technological curiosity.

- Mike's decision-making framework for investments involves identifying an upcoming market wave, understanding the technology or product (the "board"), and assessing the ability of the entrepreneur (the "surfer") to utilize the technology to ride the wave.

- Mike suggests that venture capitalists should lean into hype cycles, especially in areas that feel like inevitabilities, such as artificial intelligence.

- Reflecting on his time at Cisco, Mike emphasizes the importance of adaptability and the ability to redefine oneself and one's business expansively over time.

- Mike views being a board member as an opportunity to be an ally and coach to the CEO, helping to identify potential pitfall areas and providing guidance to navigate challenges.

- Mike's experience at Opsware revealed to him the importance of being adaptable as a leader and the necessity of a different leadership style in a smaller, entrepreneurial company compared to a larger, established one like Cisco.

- Mike's approach to venture capital at Index Ventures is deeply focused on identifying and investing in great entrepreneurs, with the belief that successful businesses are built from the entrepreneur's idea.

- Mike highlights the importance of brand management and the concept of administered scarcity, drawing from his experience on the board of luxury brand company, Sonos.

- Mike's advice for young professionals in tech emphasizes the importance of knowing one's strengths and weaknesses, pursuing a career path with passion, and positioning oneself in a role that allows the expression of one's greatest strengths.

- Mike also highlights the importance of adaptability in the rapidly changing tech industry, especially for young venture capitalists trained to move quickly in a fast-paced environment. He advises maintaining patience and wisdom in decision-making, given the current unpredictable market dynamics.

Want to know the full conversation? Read the time-stamped transcript:

The Logan Bartlett Show: Top AI investor predicts how AI wave will play out—Transcript powered by Fireflies.ai

00:00

Mike Volpi

If you just added up the dollars will flow to incumbents in the AI world more so than elsewhere. However, as a venture capitalist, we benefit the zero to 100 billion journey more than we benefit from the 100 billion to trillion journey.

00:15

Logan Bartlett

Welcome to the Logan Bartlett show. On this episode, what you're going to hear is a conversation I have with Mike Mope. Mike is a general partner at Index Ventures, where he has invested in companies like influence scale, AI, Hortonworks, Sonos, among a bunch of other very successful businesses. Mike and I talk about a number of different things, including his early career at Cisco. What made him lean in early into artificial intelligence.

00:39

Mike Volpi

There's periods of time where velocity matters more than judgment. Being fast is what matters more than being capable of assessing a situation. I think what we're entering now is a phase where judgment is more important than Velocity City, as well as how.

00:51

Logan Bartlett

He views his role as a board member and the types of investments that he looks to make as a BC.

00:56

Mike Volpi

My weakness as an investor is I fall in love with tech in the moment of like, should we do this? Should we not do this? Is pause and say, am I doing this because I love the tech, or am I doing this because we think we're going to make money at this.

Read the full transcript

01:06

Logan Bartlett

Really fun conversation with one of the legends in the venture capital industry that you'll hear now. Mike, thanks for doing this.

01:19

Mike Volpi

Great. Great to be here.

01:20

Logan Bartlett

So you were early investing in artificial intelligence. I assume it was an outgrowth of a lot of the data investments you were doing. But I think your first one was Aurora, self driving company, and then maybe a derivative of that was scale AI. Now you've invested in things like cohere, and what did you see in AI in the early days? That kind of, you said, hey, this is going to be the next frontier. This is something I want to lean into.

01:44

Mike Volpi

Truth be told, the story is a little more serendipitous than that. And I went to Ted, in fact, satish, I think, was there with me back in, I want to say, 1314. And this guy called Chris Ermson, who is now the CEO of Aurora. Back then, he was the CTO of the self driving venture at Google. It was called chauffeur. Now it's Waymo. He gave a talk about self driving, and I was mesmerized by this idea. I was like, this is incredibly cool. And I didn't really comprehend AI particularly well at that point, but I thought, well, how is it that a vehicle can drive itself? So dug into that a little bit and found out that underneath it was this deep learning AI kind of concept. And I sort of just got curious about it and started to educate myself more on it.

02:35

Mike Volpi

And I also basically started stalking Chris Ermson for the next two years, until in 16, when he left Google and ended up starting Aurora, and we did the series a there. But that was really the genesis of it. And I think what kind of sparked my interest, and I think that's still genuinely true today, which is, if you look at software programming in general, it's a representation of human logic, right? It's sort of how we codify in some thread of logic that we want to follow, but that's not exactly how the human brain actually works. And what actually fascinated me was that AI was the closest thing that we could manufacture, that looked and smelled like even today. It's not really.

03:25

Mike Volpi

I think a lot of people that draw the analogies don't quite understand how different they actually are, but it was the closest thing to comprehending how human minds work. And that's why I got fascinated by it. And then obviously, I like to align what I'm interested in and what I invest in. And so then the investments sort of followed that thread of interest that I had.

03:46

Logan Bartlett

How do you go about going down and figuring besides stock and Chris, and I'm sure following him around to different conferences and stuff, how do you go about unpeeling that like you're curious about something, and then what do you do next to figure out if there's a there?

04:01

Mike Volpi

Well, in that particular field, it's very academically influenced. And so there it was really about following the academic threads. So if you kind of go through the history of AI, right, there's a lot of work that happened at CMU, originally in Carnegie Mellon University in robotics and deep learning, et cetera. Jeff Hinton, who is largely credited today for being kind of the father of some of the modern AI concepts, was at CMU. He left and went to University of Toronto. A bunch of his students ended up permeating through Berkeley, some through MIT, some through Stanford, et cetera. So it was about kind of following that map of the leading academic thinkers in the area that sort of gave me a little bit of a roadmap. And oftentimes I actually used Chris Ermson, who was highly respect.

04:58

Mike Volpi

Kazoo is actually an associate professor at CMU before he went to Google, and his co founder, Drew Bagnell, who is still a professor at CMU, they sort of led me down the path because they had the credibility to kind of introduce me to some of these folks, and I think that really was able to kind of broaden my view around it generally. I think that's always a healthy approach to say, like, who are the domain experts in this field? And let's get to know them, right? If you're a database person, you want to know Stonebreaker because he's the guy in databases, and you sort of follow that thread of like, who are the knowledgeable people? And that gives you a map of the market.

05:34

Logan Bartlett

You are one of the few investors, I think, still active today who live through the Internet, live through the mobile shift, live through artificial intelligence. I read a quote, I was in.

05:46

Mike Volpi

Middle school, to be clear.

05:47

Logan Bartlett

Yeah, exactly. When you were twelve and you were paying attention to there, Cisco. I employed a lot of young people there. Child labor laws were a little different. But I think something you said 2015 16, comparing artificial intelligence to the Internet, which I think today, people draw that analogy all the time. But at the time, that was a little field from what people were talking about. What did you see in AI that reminded you of some of the shifts that happened into the Internet?

06:17

Mike Volpi

I think the core concept of these important shifts that happen, whether it's mobility, like with the iPhone or AI today, or the Internet of early years, social media, when it started, first came out, is that they end up kind of being these enablers, or I don't love the word platforms, but they end up being platforms where people can take them and realize new ideas off that base. Right? So if you think about the early Internet, in the early days, it was mostly about emails or message boards or something like that. Then really the breakthrough was the web, the browser and the web server that allowed people to start thinking about commerce and films and marketing and advertising. And I think it's that ability to take something that basically opens up a horizon of activities that then a subsequent group of people can pursue.

07:23

Mike Volpi

And in that context, I think the Internet and AI have a lot of interesting similarities for good and for bad. Because if you think about, I joined Cisco back in 94, and really the rise of Cisco coincided with the building of the Internet, right? They were the infrastructure for the Internet. Cisco became an important company. It was and is worth a lot of money. You could argue similar things about OpenAI, but a lot of the interesting stuff happens on top of that. And it's very hard to estimate in the moment exactly when those exciting things happen and which ones are actually good and which ones are bad. Because if you think about some of the things in the late ninety s, that we imagined the Internet would offer us. They were correct.

08:15

Mike Volpi

They just didn't happen in the time frame that we thought they would. And therefore, you have a little bit of a financial bubble that happens around it, because we all think like Webvan is going to happen next year, and it doesn't instacart happens 15 years later. The ideas happen when they happen is a little harder to judge, which brings about these sort of like bubble like behaviors. Because essentially, venture capitalists and investors in the technology business, we're all optimists. That's why we do the job that we do. We think stuff is going to happen. And that optimism leads us to sometimes incorrectly predicting when they will happen and we lose money on that. But in some cases, we're right, and we make a lot of money doing it. And that's, I think, some of the similarities that you're seeing in the AI world today.

09:01

Mike Volpi

We're envisioning the incredible things that will happen on top of AI, but we're not really sure about the timing. We're making the bets anyway. And if we're right on the timing, we'll be very successful investors, and if not, we'll lose some money.

09:16

Logan Bartlett

Is your belief then if something feels like an inevitability, like artificial intelligence in some ways, then our job as venture capitalists is to actually lean into the hype cycle and not worry too much about valuations. Within reason. Because if it works, it could be the Cisco's or the Amazons or the Googles or OpenAI today. And if it doesn't, you just lose your money. Or do you need to be pragmatic about the valuation and the price, still knowing that there's something of a mania going?

09:50

Mike Volpi

I mean, in this sense, I think you have to be optimistic, but I think you have to be careful when the valuations get very large. I think AI is super cool. I am not in the camp that says this is the coolest thing we've ever done. And if you kind of reflect that back on market caps of companies, there are a small number of companies that are worth more than a trillion dollars. There's a slightly larger number of companies that are worth hundreds of millions. Cisco, et cetera. There are more companies worth 50, and more companies worth five or 10 billion. But if you're going in and investing as a venture capitalist with a reasonable probability of failure into something that's worth 20 billion, what are my chances of making ten x on that bet?

10:40

Mike Volpi

Especially with downstream dilution and option pools, not super high. There's one company every five years, or one company. And what are the chances? This is it's pretty low. And so my view is at the lower valuation ranges, 5002 hundred, even 510 x is a $5 billion company. There's a reasonable number of those. And so you're like, statistically speaking, I have decent odds at making this one work, but you go to the roulette table and you just bet one number, the chances are you're not going to get it. And I think that while I think it's smart for venture capitalists to lean in, it's smart for us to have a portfolio in AI because we don't know which one's right. And it's smart to be moderated on the investment, the entry point of that investment, in order to sort of accommodate a reasonable failure rate.

11:38

Logan Bartlett

Do you think, having lived through those platform shifts, Internet and mobile, and I guess now AI, do you think that makes you better equipped to have the prepared mindedness and some of the historical precedents of how some of these things have played out, or does that lend itself to some level of cynicism and there's going to be more optimists out there that will see things differently and say, no, this time is different.

12:11

Mike Volpi

Well, I think the first thing it helps you is to identify the real waves and the not so real waves. I've been a skeptic and I was quite a skeptical about the whole crypto wave, so didn't really do any investing in that area.

12:24

Logan Bartlett

Were there specific things that you saw? I mean, I was as well, but.

12:27

Mike Volpi

I'm curious, because when we call it a platform, what we're saying is it enables you to do a lot of things that you couldn't do before. Right. That's kind of the point of it. I never figured out, other than speculating on rising crypto prices, I didn't understand what it is that you could do that you couldn't do before. Arguably, with maybe if you live in Argentina, it's a good deal to have some of those, but it's not enabling. Right. It is a currency in and of itself, so the identification is helpful. So you see these waves and you go, this is going to be important. So just a recognition, when you recognize it, trying to get in early before the prices go sky high, that's super relevant.

13:10

Mike Volpi

And then sort of trying to understand how to capture value around that platform shift that's happening, I think, right now, when you hear a lot of venture capitalists talk, they're talking know, is this just a wrapper on OpenAI or on cohere or on cloud or something like that? Or is there a real company here being able to identify the difference between just a wrapper and an actual app? Those are the sorts of things that I think help you that I can take lessons from. The Internet era, like email never really was a great business, but a website that does commerce was. Even though technically you're saying, well, how hard is this? You're just moving bits from one place to another. But there was value there.

13:55

Mike Volpi

So being able to identify where there is more than just a wrapper is, I think one of the skill sets that carries over from generation to generation of waves.

14:05

Logan Bartlett

Is there a distinction or a question you'll ask that are between a wrapper one side and a net new application that could create equity value on the other?

14:17

Mike Volpi

Well, specific to the AI world, a lot of times I try to comprehend how much does this particular app embrace details of the use case of what the user is doing with the app, right. And how much of it requires knowledge of a specific domain. That domain could be human resources, it could be marketing or sales, it could be the automotive industry. There's a lot of domains, but most oftentimes SaaS applications have to capture the essence of that user's workflow. And ideally in many cases it occupies the workflow of more than just one person. It's not like just a single player productivity tool, but things that make things more than wrapper are many people use it and they benefit from the network effects of using it together. There's specific embedded knowledge of the workflow of the user in that sector.

15:21

Mike Volpi

There is an intelligent usage of multiple types of underlying capabilities of the model. So maybe there is a vision thing or this kind of language model for this, a small model for that, a big model for that type of thing seems to me the key to finding what is not a wrapper and an actual application.

15:43

Logan Bartlett

As I think about maybe the Internet versus mobile, and I'm going to make these numbers up and maybe you'll disagree, but Internet, I think 90%, maybe 80% of the value that got created by the Internet were net new companies that got created, be it Amazon, Google or whatever. We can go down the laundry list of names, they're still Microsoft's and things that ported over some of that value. Mobile, it felt like the vast majority of the equity value that was ultimately created was captured by Apple and Google in large part. And then there was Instagram and Uber and a bunch of others as well. Do you think that the equity value within AI is going to be captured by a lot of the incumbents with the existing data, and there'll be a handful of those that create new value.

16:35

Logan Bartlett

Like how much do you think it's closer to the Internet where maybe it'll be a ton of net new equity value created by startups versus mobile, that a lot of it gets captured by existing vendors?

16:45

Mike Volpi

Yeah, well, I think in that sense, if you compare the Internet generation to the current AI theme, my suspicion is it'll be a little bit different in that the current competitors in AI are quite competent. Google, Microsoft, Amazon, Apple are companies that are still on it. They haven't sort of lost the plot, as was the case maybe at the beginning of the Internet. So a, it's likely that they're going to capture a big chunk of the value. Second is the point you mentioned, which is they have a very interesting data advantage and whether it's good or bad data is a good question, but they certainly have the wherewithal to capture that advantage. And the third is the capital intensity that AI requires. And that's also a slightly different theme than the Internet didn't require.

17:39

Mike Volpi

It required capital for telcos to build out infrastructure, but nowhere near dimensionally what we're seeing here. So there's a capital mode, there's a data mode, and there's just a competence mode that incumbents have. So my guess is in the end game, if you just added up the dollars will flow to incumbents in the AI world more so than elsewhere. However, as a venture capitalist, we benefit the zero to 100 billion journey more than we benefit from the 100 billion to trillion journey. And so I believe that there will be enough interesting companies that look like Uber or Insta or whatever the case may be, that benefit from the existence of that mobile platform and will create ample opportunity for upside for venture capitalists.

18:34

Mike Volpi

So there's, in other words, even if they're not the biggest allocation of dollars, there's so many dollars that I think our industry will do well out of it.

18:42

Logan Bartlett

I heard you say at some point large language models will be commoditized and so it's all going to be about the data that you train it on. I guess one, do you remember saying that? Or the context around it?

18:55

Mike Volpi

I was probably wrong, but yeah.

18:56

Logan Bartlett

Okay. Can you elaborate on that point or how you sort of think about the value that might go to large language models and the data and all of that?

19:05

Mike Volpi

Yeah, well, I think it's a nuanced thing, actually, and none of us have a crystal ball we're learning every day. But broadly, I would segment in two ways models, if you really distill it out from 100,000ft, perform better based on two things. One is how large they are, and two is how much good data they have to train on. Those are the two big axes. Large models cost a lot of money. Having lots of good data costs a lot of money. And so at least if I were to give you my snapshot of my crystal ball today, I would say is you're likely to have two or three sustained leaders in the large language model space, particularly as applied to consumer applications. It's likely to be OpenAI, it's likely to be Google, there might be a third in there, who knows?

20:01

Mike Volpi

And that will largely serve the more consumer universe. And even if you look at OPA's revenue, the vast majority of us is all of us paying $20 a month to them. There's that part, I think that there are a lot of functions that will go basically use AI to enable sort of enterprise applications, and that's going to be a bit of a different dynamic, because those enterprise applications, if I go back to the point I was making earlier, will have a lot of domain specific knowledge and data that will allow even a smaller model, which is cheaper to serve, cheaper to train, et cetera, to actually perform important functions in the enterprise. So I think you're going to see a divergence in the market between the consumer side of the market and the enterprise side of the market.

20:47

Mike Volpi

Now, on the enterprise side of the market, the interesting risk is like, is there some commodization going to happen? Because you have a lot of open source models that are out there, and maybe there is that possibility that the open source models will tend to drive the price points down and commoditize the enterprise side of this. I think there's still some, it's not all self evident, because there are some rough edges to the open source models that don't make them incredibly enterprise friendly at this point in time. So we'll have to see how that plays out. But broadly, I see kind of that segmentation. I think given the capital required, it's hard to imagine, mean, I think there's going to be significant price wars between OpenAI, Google and whoever else. Because if you're Google, this is truly existential, right?

21:35

Mike Volpi

It's absolutely existential to win this market. They will throw everything at this. And so I think what you're going to see is some amount of price war, I. E. Commoditization but around a small number of players, not a complete disappearance of value because everything is free.

21:52

Logan Bartlett

Makes sense. I guess one of the things that's atopic de jour, it seems like these days is AI regulation. The existential threats around AI. Do you have any thoughts on what role should the government play? What role should private sector play? Any opinions about that stuff that seems to be playing out daily right now?

22:16

Mike Volpi

Yeah, I mean, it's a complicated subject. I have not historically seen our government, and these days as functional as our government is be able to create regulation that keeps up with the velocity of technology. I agree with some of the first principles that are being laid out right now, that it shouldn't be discriminatory and it shouldn't do these bad things in general. What I actually believe more is that when you look at the people that are providing the leading edge models and capital and so forth, they are ultimately pretty responsible companies. Microsoft is a responsible, I don't like everything that they do, but broadly a responsible company. So is Google. And I am more inspired by the fact that the cutting edge is being done by responsible companies versus there's some wonderful regulation that created that safety harness around it.

23:14

Mike Volpi

I will say that there is risk in the open source universe because if I'm a bad guy and I want to build a nuclear weapon and I have a really good open source model, I can probably sort that out. There isn't an obvious regulation that I can think of that would be effective to say let's stop that. Right. And I just think that we're going to have to move along the journey and hope that the right actors do the right things to make sure that technology is used in the right way. Eventual regulation, no issues with at all. I just don't think it's going to happen in the timeframe that the technology is moving at.

23:55

Logan Bartlett

Over the course of your career, you've made investments in everything from hardcore infrastructure. We talked about Aurora scale. You've also done some consumer investing. Blue bottle, you're an investor in Sonos.

24:05

Mike Volpi

As well, is that right?

24:08

Logan Bartlett

What's the through line across these investments? What's a Mike Volpe investment in an entrepreneur that gets you excited about.

24:15

Mike Volpi

It's really just completely.

24:17

Logan Bartlett

No, just cherry picking randomness as it comes across.

24:21

Mike Volpi

No, I mean, I've always thought, know as a at you look at your balance Sheet like what are my assets, what are my liabilities? And for me at least, I think I have two assets. One is I'm very curious about technology and so figuring out investments that tickle my curiosity, whether it's data infrastructure or it's AI or whatever, I pursue it. So that's one thread, and then the other one is, I have a network of people that I love working with, and I have over the years, and I lean in on that asset when I know I have a special person that I'm working with. So if you take, like, a Sonos, the founder of Sonos, who led us to making that investment was a guy named John McFarlane, who I'd gotten to meet back in my Cisco days.

25:13

Mike Volpi

He founded a company called Software, went public, very successful, and he called me up and know, you should look at this. And was completely off the roadmap. We weren't going to do music stuff and hardware, but it was, you know, blue bottle coffee, which is this entrepreneur named Brian Meehan. Brilliant entrepreneur. I met him. He was my neighbor in London. I met him. I thought, this guy's super smart. He called me up one day and said, you want put money in blue bottle coffee? And I was like, well, anything Brian does will do. So it's sort of like the two threads are amazing people that I've gotten a chance to meet in life. Another one would be wealthfront andy Rackliffe, who I've gotten meet. And then the other one is stuff that tickles my technological curiosity. Those are the two threads.

25:55

Logan Bartlett

What's your mental underwriting framework or decisioning process for getting to the point of saying yes? Are you instinctive in the way that you sort of know when you first meet it, or are you peeling back the layers over and over again and really yearning and agonizing about getting to a yes?

26:14

Mike Volpi

Yeah. Listen, I like to use analogy when I talk about this one. I'm not much of a surfer, but it's a surfing analogy. I think there's three things that you have to convince yourself that you have, right? A surfer needs a wave, a board, and he or she who surfs. So there's the person, the board, and the wave. The wave is you kind of want to look at a landscape and see something that's actually changing in your favor at the right time. Right. If you look at quantum computing, interesting theme, not happening right now. There's no wave, right? AI, clearly big wave. So first identify that there's a wave coming. Usually the wave is an externality, meaning you don't control it.

26:55

Mike Volpi

The only thing you can do as a company is to time getting on the wave at the right time, but you're not making the wave. That's one. The second thing is the board, which I think of it as the product or the technology of the company. And do you have the correct instrument for that wave at that point in time? And again, this is like, the correct instrument means you need to have good technology. But technology is defined as good to the extent that it solves the problem it's trying to solve. And so that's the instrument.

27:27

Mike Volpi

And the last one, which is ultimately probably the most important, is the surfer themselves, who has to be able to figure out that, I need to take this board and put it on this wave at this time, and then navigate the weirdness of that wave, because that wave has competitors in it. It has early adopter customers, late adopter customers. It has macro climates. People don't want to spend money, do want to spend money. What you try to look for is a great entrepreneur who knows how to use technology to take advantage of a wave that's coming their way. Right. And if you have all those three, then you have a winning investment. If you have only two, you need to think hard about it.

28:05

Mike Volpi

In general, of the three, my biggest bias is almost always the founder or the entrepreneur, because I think entrepreneurs are good at identifying waves. They're good at identifying which technology you need to use to tackle it. And so they find their moment in time. But you see a lot of fantastic entrepreneurs who are just sitting out there on board with no way.

28:26

Logan Bartlett

Yeah.

28:30

Mike Volpi

You got to think through that. That's probably the most important element. But ideally, you want all three when.

28:35

Logan Bartlett

You'Re actually going about diligencing a deal. How does index do it? Do you guys pair up and have two people prosecuted? Are you sort of on your own hunting? Do you have a junior person helping you? How does that kind of work?

28:48

Mike Volpi

Yeah, generally we have a team effort. Usually you have a partner and a secondary partner that are working on it together, and we have a team of younger folks on the team that help us out. So it's usually a team of three or four folks that are working on any particular transaction.

29:08

Logan Bartlett

I heard you say that 80% of your investments are ones with good confidence. You'll make money, which allows you to do 20%, which are the moonshots. And who knows? How do you sort of think about what the 80% is versus the 20%? Is that something you actually articulate internally? Like, hey, this is one of my 20%?

29:27

Mike Volpi

Yeah, no, I think my partners know about it. But, for example, I've had good success in my career investing in a lot of open source data infrastructure companies. Hortonworks, Cloudera, elastic, confluent, Clickhouse, now cockroach labs, Kong et. I'm a student of the mechanics of how that works, how you turn it into a business. And I feel like, okay, that's middle of the fairway for me. I know how this business works, I know what to look for, I know how they monetize. And for me, they've produced five to $15 billion outcomes as market cap companies. And sort of that's kind of what I think of as my 80%, like, stay in the lane.

30:17

Mike Volpi

If I produce that output for my partners, which generates returns for them, generates return for the lps occasionally they're going to let me do some crazy shit which is like self driving cars or robotics or early investments in AI. And so I think as an investor, I like to have a little bit of that balance. And that, I think gives me a platform to do crazy things. And sometimes those crazy things, they work out, or even derivatives of those work out, right? Because Aurora has been a good investment for us as a public company. We've made some money on it. But I made the scale investment because of Aurora. And scale's turn to turn out to be a fantastic return for, you know, the crazy things sometimes lead to good stuff later.

31:05

Logan Bartlett

Yeah. Hey, guys, I'm Jacob Efron, a partner of Logan's at Redpoint. Wanted to take a quick break from the episode to let you know that Redpoint's AI podcast, unsupervised learning, now has its own YouTube channel. We have an incredible set of guests, really at the forefront of the AI revolution. So if you're interested in what's happening in AI, what it means for businesses in the world, definitely subscribe now back to the show. I'm curious actually, because you bring it up in scale. I was going to ask this later, but Alex was 19. I think he was 2020 when you invested him. What did you uniquely see in him? I've sat down and done a podcast with him and he's obviously a fantastically intelligent, sort of cerebral individual. But investing in a 20 year old is a risk in and of itself, I guess.

31:51

Logan Bartlett

What did you see in him at that time?

31:53

Mike Volpi

I mean, first of all, as far as Alex, I can wax poetically about what an amazing entrepreneur he is. Everything you want out of an entrepreneur, he's twitchy, restless, he's incredibly smart, he's super commercial, he works his ass off. He's a great networker. He sees technology before it arrives. He adjusts and shifts. I mean, so many good qualities were.

32:15

Logan Bartlett

Those things that you intuitively knew at 20 years old? Or are those now that he's 26 or 27 or whatever?

32:22

Mike Volpi

No. And actually I think that's the interesting part of your question, which is that when you invest in a 45 year old, you more or less have the final product. That is what that person is going to be. When you invest in a 20 year old, it's not a finished product. It's got rough edges. You're not sure about this. I think what you have to do as a vc is to sort of squint and ask yourself, this person looks like this at 20. What will they look like at 25 or 30? Can you extrapolate the trajectory of this individual? And it's really hard because humans change enormously between age 20 and age 30. It's a life defining decade for us. We find our motivation, our ambitions, our aspirations. We face our first challenges as an adult. And so the extrapolation is inaccurate at best.

33:21

Mike Volpi

But you try your best to see what this person is going to turn into. And I think honestly, being a parent of somewhat older children is helpful in that assessment because I've seen my own kids evolve and change and become different kinds of people. So I think that's an art form. I don't always get it right, but I think oftentimes when I read briefing memos from vcs, it always says, this is what the entrepreneur is. And it never talks about what is the entrepreneur going to be in five years. And I think that's a bit of an art form. And if you look at the greatest returns in our business, whether it's an Amazon or a Facebook or whatever, oftentimes you see the leader evolving a lot as a leader in time.

34:07

Mike Volpi

And it's funny how we don't actually pay attention to it, we just look at it very statically.

34:12

Logan Bartlett

Yeah, I guess it's much easier to take that snapshot than it is to try to project the person. In some ways, I guess I think the projection can lead to maybe some level of false precision. I've always found that the in between when you write a check and then you sort of go quiet for four weeks or whatever after, and then you go to your first board meeting and the entrepreneur has been through a bunch of fundraise conversations and how much they've changed by the time your last conversation with them to your first board meeting or whatever with them is usually a pretty good sign of the slope of the line and how quickly they're going to grow.

34:49

Logan Bartlett

I guess that's one of the things of getting to know entrepreneurs over long periods of time and getting them to see them evolve as you have those conversations.

34:56

Mike Volpi

Yeah. And there's always this kind of question about where is the value that a vc brings to the table. Right. And it is true that a lot of what we do is just invest. That's our primary act. But I think when you're investing in a 45 year old leading or a group of established founders, you are more along for the ride when you're investing in a 20 year old, and I've experienced this firsthand with Alex or George Sivulka at Hebia and so forth, is you are shaping who they become also. And I find that absolutely fascinating. It's an absolute privileged position to take these incredible people who have so much talent and to be able to sort of unlock aspects of them. Mostly they're growing on their own, make no mistake.

35:50

Mike Volpi

But you can clearly feel your influence much more than what you can do. You give a nice piece of advice to a 45 year old, but they are who they are.

35:58

Logan Bartlett

Yeah. You started full time investing in 2009. You went over to index, but then you were investing in the Cisco when you were twelve years old. Going through that stretch, if you could go back in time maybe to when you started at index, what's something you know now that you wish you could have told yourself then about investing, about working with entrepreneurs so much?

36:27

Mike Volpi

First of all, I think it takes a while to become a decent venture capitalist. It's not a profession that you can write down and explain. I mean, I'm sure you know this, but it's very experiential and I think it's artisanal in its nature. You got to understand a lot of different details of how things come together. Probably most of my professional career prior to going to work for index was operational in nature. I had done some investing, and I think probably the first thing I would tell myself back then is actually let go of some of those operational first principles, because I think operators tend to think too much in the first person when they look at a company psychologically, you're like, if I had this product and this market, I could lead this company to win big.

37:25

Mike Volpi

Problem is, it's not you, it's another person that's doing it. And so you have to kind of let go a little bit of your sense of analytical structure of how is this market structured, what is the competitive nature of it. Can I do due diligence on the technology and embrace more the understanding of the person, of the founders and their ability to execute against that idea and that technology. So that was probably, I was more focused on markets, on competitive dynamics, on technology, and less focused on the people. And over the last 15 years that I've done this, I've learned that it's more about the people and a lot less about the technology. The technology is important and so on and so forth. So that's probably the biggest shift, I would say, that I've tried to internalize.

38:20

Mike Volpi

And then the other thing is, this is a pattern recognition job. And so it is about seeing an opportunity and saying, do I have any other situations where this pattern has repeated? And I can sort of follow that trend? And that's true both in terms of the business opportunity, but also the individual founder. Now, founders are hugely diverse. There's all sorts, but there are patterns. Right. And so can I see a pattern in this person? And those are probably things that I didn't really understand super well when I got to the job day one, in.

38:56

Logan Bartlett

Talking to a few folks at index, more than one said that you were the best mentor they've ever had in their careers.

39:06

Mike Volpi

They must not have had very good careers.

39:08

Logan Bartlett

Yeah, well, it's a limited number of people, I guess, they were working with.

39:11

Mike Volpi

We do pay their salary.

39:13

Logan Bartlett

Yeah, exactly. I'll tell you the names after they were maybe looking for a pay bump. So when you think about developing young venture capitalists or helping them learn this artisanal craft that comes with experience and all the sort of some of the things that you've learned over the course of the last 15 or 25 years, or however you want to score it, how do you think about nurturing those people and helping them find their own lane? Because what's true of Mike Volpe, what's true of Doug Leone and Peter Fenton and Mike Moritz and all these people that are iconic names in the industry is going to be slightly different. Right. We're all sort of throwing different pitches. We're doing things slightly differently. But how do you help pull out the best of the people that you're working with?

39:59

Mike Volpi

Yeah, I mean, there's a lot of things, but I'd highlight two, which is, first, in the venture capital business, you have a lot of very hardworking, very intelligent, talented people. This is a very high density of that type of profile. That type of profile is best managed or best mentored by giving them a lot of free space and allowing them to take risk. Right. The core thing is jump into the deep end of the pool. I think that the best people shine the most in that circumstance. And the venture capital is populated by a lot of smart people, the ones that have performed very well, are few and far between. But all of those, you just wanted to throw them into the deep end of the pool. What does that translate to?

40:53

Mike Volpi

It's like, pick a sector and you go invest in that sector and let me know how I can help. So take like one of my amazing partners at index, Shardul Shah. He joined us in the US team. He was the first person we hired on the US team back in 2011 and we didn't really have a person covering security. And I was like, okay, Shardul, take security, it's yours. Go build a network, figure out what to do your investments. I'm here to help, I'm here to open doors if I need to, but really it's about giving them the freedom and the flexibility and most importantly, the self confidence that they can tackle whatever problem is faced in front of them. That's one dimension.

41:35

Mike Volpi

The other thing that I try to do is not give people answers, but give people frameworks to figure out their own answer. So you ask me, I have this problem, should I invest in this company? I'm not going to tell you whether you should invest in the company. I will give you a way to think about whether you should invest in this company and then you are in the details. You know the people better, you've studied the market better, whatever, you have all the data. I'm going to give you a framework like the one I just gave you about the surfboard and hand you that framework and saying, you figure it out and I'm going to back you up. And by the way, look, as a vc, maybe you're better than I am, but I don't think I get half the time. Right.

42:17

Mike Volpi

And so you better get used to letting people make mistakes. I've made so many. And as a venture capitalist, it's sort of like it completely comes with the territory. So letting people feel like they should not fear making a mistake, if you went through a rational process using the right frameworks, you came up with the answer, you invested, the company didn't work out, it's fine, it's totally fine, just go back at it, right? As long as you're using those frameworks. So don't quibble with the decision of whether you did or did not do a right thing. Just focus on the fact that you use the right mental frameworks to make the decision that you did.

42:56

Logan Bartlett

The mistakes you've made, are there commonalities or through lines between them that you've now learned? Of course. Correct. Maybe you invested too much in the board and not the wave or anything along those lines that you've looked back and you're like, I wouldn't have done that again because we're always going to be wrong, right?

43:17

Mike Volpi

Just statistically for sure. I think, look, one of the most important things we understand we have to do as people is to understand our own weaknesses, right? What are my pitfalls? And in some ways, those are often the flip side of the coin of your greatest strength. So I said earlier, I love tech. My weakness as an investor is I fall in love with tech. And so what I have to do, oftentimes in the moment of like, should we do this? Should we not do this? Is pause and saying, am I doing this because I love the tech, or am I doing this because we think we're going to make money at this?

43:53

Mike Volpi

And the most frequent problem, mistake I've made in my career is just falling in love with the technology more than falling in love with the business and the people and all that good stuff. So that's what I have to guard, ban myself against. Although that's just me. Every one of us has blind spots. And so the most important thing is just recognizing what's yours and then surrounding yourself with people, or surrounding yourself with frameworks that prevent you from going off the rails. Given that blind spot, is there an.

44:25

Logan Bartlett

Investment that stands out that you didn't make that's particularly painful? I'm sure there is. We all have them. I can think of a list of five of them or something. But that you tweaked your mental model going forward saying, hey, I was off on this, and it's something I need to think about going forward.

44:44

Mike Volpi

Yeah, I mean, I'll cite one that gives kudos to Redpoint, which is Snowflake. The first investor in Snowflake was Mike's pisor at Sutter Hill. Credit to him, he was kind enough to show us and me the series b, and then probably a number of subsequent, you know, I sort of used market logic to convince myself it wasn't a good idea, because it was, you know, Amazon has redshift. It's their fastest growing, most competitive product in the market. This is just analytical database. There's lots of those. There's Netiza and Vertica and teradata and all these. Technically speaking, it was more scalable on a cloud basis, but I sort of essentially used market logic to talk myself out of it.

45:39

Mike Volpi

And what I didn't appreciate, for one, Binon, the founders there, who were amazing and then the ability that Mike had to bring in, first Bogmuglia, who was a great leader, and then Frank Slutman, who was also another great leader to evolve the company just didn't enter my framework know, but those ones hurt.

46:03

Logan Bartlett

Yeah. No. When you're wrong on things that you invest in, it goes to zero. When you're wrong on things that work out, they go very far.

46:15

Mike Volpi

You can only lose your money once.

46:16

Logan Bartlett

You can lose it once. You said something that I found pretty profound. I'd like to read back to you and get you to elaborate on, but most companies and people define themselves and who they are in too narrow of a way. When you're getting started, it's important to focus, but then over time, you need to redefine yourself more expansively. Can you elaborate on that sentiment, either for companies or people?

46:39

Mike Volpi

Yeah, I mean, that was sort of my big lesson in my first adventure in a professional life at Cisco. I joined the company when were about 1000 employees, I think something like that. And seven years later we had 50,000 employees. And I think the company succeeded in many ways because it kept reinventing itself with additional chapters too. First it was a router company, then it was a router and switch company. Then it was an Internet working company. Then it was like it kept reinventing its existence. And in some ways the phrase I often try to use is like we sort of define the sandbox of what it is that we are, and we try to excel within that sandbox, but then we ultimately just live in that sandbox and we forget that the whole point is to make the sandbox bigger.

47:31

Mike Volpi

That lesson applied to Cisco. I think it really applies to people a lot, especially capable people, many of them in our business and venture capital, but also in other professional walks of life that define themselves as, this is who I am. I am a programmer, I am a salesperson, I am a marketeer, I'm really good at Java. And you kind of in the moment feel good because you excel at this thing which ultimately actually doesn't fully expose who you are as a person. And so being able to sort of assess where you are and say, you know what, I'm going to make that sandbox bigger. I'm going to try something different. I'm going to try to expand my competence that allows us to really fulfill our full potential. I was not a software engineer, right? I programmed, but I was mechanical engineer.

48:31

Mike Volpi

And if someone says, like, how does mechanical engineer understand anything about AI? Probably, right. But then if you just sit there and you read papers and you try it and you download the software and so on and so forth and you redefine, you say, well no, it turns out I'm not a mechanical engineer. I can understand this other stuff and I can understand this other stuff over here. You gradually expand the sandbox. And I think it's not such a blind process because if your sandbox is two x four and you sort of say, I'm going to go to 30 x 50ft, not so much. But there's a gradual process associated. But it's really important for people to continue to grow. I mean, another way to put it is this whole growth mindset mentality.

49:17

Mike Volpi

But I kind of think of it as expand the domain in which you can act to allow yourself to learn new things and excel at more things.

49:26

Logan Bartlett

Similarly, you said evolution has taught us that mistakes are bad, but that's not true, which is a weird thing, especially as a venture capitalist, you need to be willing to make mistakes so that you can hit the ball far out of the park. But how do you think about that?

49:44

Mike Volpi

Look, I actually think the VC job is very statistically oriented job, right at the end of the day, much as a baseball player goes up to the plate and tries to hit, if you're really good, you're going to hit it. They're about 33% of the time, but if you don't swing, you're never going to hit it. And so I do think that it is absolutely critical to embrace the idea that mistakes are part of what you do. It's fine. And before even saying like, I learned from my mistakes, that's kind of obvious. It's just forgiving yourself for your mistakes. Like saying it's fine, it's totally okay to make a mistake. And if you're not, it's probably worse, right? If you make no mistakes at all, you're sitting in that small sandbox and just bunting every time the ball comes at you, right?

50:34

Logan Bartlett

Yeah.

50:35

Mike Volpi

So making mistakes comes with the territory when you expand it. And then obviously you try to learn from your mistakes. But some of your mistakes, the lessons you learned are pretty obvious. They just show up and you're like, I'm not doing that again. Yeah. But I think the most important part, and I think particularly for very competent people, you hate making mistakes, we hate making errors. It's interesting because it's a human thing, right? 10,000 years ago, when I came out of my cave and I did it at the wrong time, the lion ate me.

51:16

Logan Bartlett

You died.

51:17

Mike Volpi

It was really bad to make that, to make a mistake. Mistakes translated into tragic endings. Today, professional mistakes. People give us 3000 shots. And so I think we overweight the idea of making a mistake in our own mind. It's a sort of psychological factor. And I think the most important thing is just to let it go. Like, all right, fine, screwed it up. Let's move on. Try again.

51:46

Logan Bartlett

So there's a book called done deals that was written in 1999 that I read when I got into the venture industry. And I actually still had sitting on my bookshelf. And I went back, and I remembered there was a chapter that you wrote about when you were at Cisco and Cisco's investing strategy. In there was a comment that you made about getting credibility with entrepreneurs, and there was two people you referenced. You said, you can call them and ask about me and ask about Cisco. And the two people were Don Valentine and John Dore, two of the most prominent people in, I think, our industry's history. What do you remember about both of those people, their style? Were there things that you internalized about interacting with them that you carry with you today?

52:32

Mike Volpi

Yeah, I mean, the interesting thing about those people is they, in some ways, interestingly, represent the venture capital business. Both are not active vcs now, but in their era, they were the titans of our industry, and they were completely different human beings. Don, unfortunately, has passed. John is still active, doing a lot of really amazing philanthropic things. But Don was a guy that he would show up at the board meeting. He had his little sequoia notepad with a green pen, only green pen, and oftentimes he wouldn't talk. He would just write notes and hand them to you. And he commanded extraordinary presence. And he was the guy that you were completely afraid, know, saying something stupid. Now.

53:18

Mike Volpi

He also had this uncanny ability to see a situation, a person, a threat of logic or whatever, and see flaws, chinks in their armor, and use that to go drill in and figure out what's really going on here. John was enthusiasm drive, his contagious sort of ability. In some sense, he was an entrepreneur himself, that he sold you the vision, right? Both turn out to be very successful at what they do. And the lesson you take away from it is that there really isn't a mold for a successful venture capitalist. There's those two. There's Mike Moritz, who was a journalist. There's Peter, who is, I think, fourth generation vc or something like he's sort of born in bread at birth. He started writing checks to people. So you have this huge variance of how you undertake the task of being a venture capitalist.

54:12

Mike Volpi

And the big lesson from those two was how you have to actually design your own approach as an investor in doing it in your own way. You can also inspire others. And both of them were very inspirational. Both of them also, I think, for me at least, were extraordinarily generous with their time. And when you think about it in reverse, I was some kid that's 26, 27 years old or something, going up to Don Valentine, one of the greats, or Dora, one of the greats, and being like, hey, can I grab lunch with you? Sure, come on in. Talk anytime you want to come by for advice. Come on in. And so you got to pass that down to the next generation. And the way I think of it is like, I've had some reasonable success being a venture capitalist.

55:01

Mike Volpi

When some kid calls you up and say, hey, can I grab lunch? Yes, absolutely. Then you can make your assessment as to whether that person is worthy of more time or less, but keep that door open as they did for me and hopefully I've done for others and hopefully many people will continue.

55:18

Logan Bartlett

There is a comment you made in that book about recommending buying the market leader instead of the lesser players despite paying a higher price. I think the quote you had was the right way to frame the question is not how much you're paying for an equivalent asset, but rather how much better can the market leader perform when combined with the asset of the larger company. Is that something you think about today investing, paying a premium for the market leader rather than going in for the number two at a lesser price?

55:49

Mike Volpi

Absolutely, yeah. I think that we live in an industry where the leader gets 70, 80% of the value. I think the concept of the cheap and cheerful number two doesn't work in our business. And at index, we've seen the same thing where we invested in a number two player and occasionally you get a decent return, but by and large, investing in the number one player. I think in that context I was speaking more about M A and I still that I think that is absolutely true, where if you're going to buy somebody to integrate them into your company today, it's much more difficult because there's a lot of regulatory issues and so forth. 100% pay more. What people forget is that you're sitting there saying, company a, market leader, 200 million dollar valuation. Company B, second place in the market, $50 million valuation.

56:48

Mike Volpi

In one case I own 15% of the company, in the other case I own 20% of the company. For a little less money, five years later they go public. You will make or lose more of that intraday trading in the stock price. So you're fixated on complete. If you really believe that the thing is going to be public, or if you really believe that this particular acquisition will transform your business in some way, you're completely crazy to think that plus or -20 or 30% of the price makes any difference when you invest or when you buy in the company. You're focusing on super micro instead of like the big picture of what's going to happen over a longer time horizon.

57:27

Logan Bartlett

Yeah, and that's even from an m and A or a return standpoint. And then there's the benefits of the reference ability of being in the market leader as well, which is very beneficial to at least our job, right, being in the number one versus the number two for sure.

57:48

Mike Volpi

I mean, I'll give you a concrete know. I was fortunate enough to enter this business with a little bit of a brand and a reputation when I entered it. But that wasn't to say that I was going to be any good at investing. One of my first investments that I did with Satish, with pure storage, right, pure storage. And I want to say we did the series, maybe C or D in the company at a pretty high valuation, like 500 million dollar valuation. I forget how much money we put into it. So I wouldn't say this was like a premium, whatever, but fast forward, I think pure storage today is worth, I don't know, 15 billion something in that neighborhood. So clearly a perfectly good investment. And then you start to build a brand.

58:36

Mike Volpi

Know, Frank Slutman's on the board, Anil Buster is on the board, satish spiser, you've got this really great group of people that are like, hey, that guy Volpe, he's all right, he knows what he's doing. He invested in this. And then people like pure stories, this, that, and then that opens the door for the next thing, which I think was Horton works with Fenton, and that opens door to the next thing and the next thing. And so playing with the, as you're getting started, somehow being associated with the winner. And of course it's not just making the investment, you got to work hard after that for the company, but that sort know gives you the platform to do a little bit better and a little bit better.

59:16

Logan Bartlett

So shifting gears a little bit. You were born in Italy and then grew up in Japan.

59:22

Mike Volpi

Yeah.

59:23

Logan Bartlett

How does someone born in Italy, growing up in Japan, end up in California in the middle of the Internet bubble?

59:31

Mike Volpi

Well, it's kind of serendipity. I was born in Milan, Italy. My dad worked for local bank when I was six. My mom and dad were kind of the adventurous type, and so the bank offered them expat, job transfer tokyo. They took it. I started first grade in Tokyo, and I had this kind of an eclectic life of going to an american school in a society that was totally different. Made some really interesting friends along the way, because a lot of the other kids that I went to school with were sort of like me, kids of executives at IBM, kids, diplomats kids, whatnot. And then I liked science and math. And so because the education was in English, when I got to applying to college, going to America was sort of the obvious thing. And then I applied to a variety of american universities.

01:00:33

Mike Volpi

Several of them were in Boston, and one was in California. And I visited in. So truth be told, the know, I drove down Palm drive, and I was like, wow, this is nice.

01:00:44

Logan Bartlett

This is different. Yeah, that's good.

01:00:47

Mike Volpi

So that led me to the Bay area. And I think after a few years, even as an undergrad, I started to recognize, wow, there's something very special happening in the field that I love in this area. And obviously, it became infectious after that.

01:01:05

Logan Bartlett

Going from Italy, first grade to Japan. Is that right? Yeah. Do you think that has helped you in being able to resonate with different people and get along in different environments?

01:01:17

Mike Volpi

Yeah, 100%. I mean, probably the biggest takeaway lesson is adaptability, which is being able to change yourself a little bit to adjust to the environment. But I think the less obvious one is being able to see things from another person's perspective. Where I find it's most useful is in negotiations. Oftentimes you're negotiating, it's a term sheet, it's an m and a transaction, whatever. The thing that I find most useful is I look at the problem from the other person's perspective, and I try to orient where we're going to fulfill what's important to them, which is oftentimes not exactly what's important to you, or in some cases, I want them to get them to see the world a little more the way I see it.

01:02:11

Mike Volpi

So how do I change their prism a little, but the ability to see things from another person's perspective, obviously being thrown from. And by the way, Japan and Italy, there are no two countries with more diametrically different cultures. It's crazy how different they are, but you sort of have to adjust to that and see things from the other person's perspective. And that's know, a good lifelong lesson for me.

01:02:35

Logan Bartlett

Would you walk into an italian home and then walk out to a japanese culture. Is that sort of the. So you're flipping context?

01:02:42

Mike Volpi

It was a three way context flip because my school largely, I'd say my high school experience was comparable to any american kids. But I had friends in the neighborhood. I spoke Japanese. I still speak Japanese. I had japanese friends that were local neighborhood kids. And then at home it was pasta and Osabuko.

01:02:59

Logan Bartlett

Right. Probably a little louder at home, too.

01:03:03

Mike Volpi

Yeah. But honestly, it's one of those strange things. I think this is the beauty of like, didn't really think much of it. It was only when I got to America that people were like, wow, that's really unusual. And I was like, I guess, yeah.

01:03:14

Logan Bartlett

You'Re fish and water the whole time. You don't really appreciate it.

01:03:18

Mike Volpi

Exactly.

01:03:19

Logan Bartlett

So you graduated Stanford in 94?

01:03:22

Mike Volpi

No, I finished my undergrad in 88. I stayed an extra year, got a master's degree in 89, and then I went back for my MBA and I finished that in 90.

01:03:31

Logan Bartlett

Okay, got it. So that was your business school. Fortuitous timing to be graduating. I assume that was. Internet was starting to take off. Had Netscape been started then?

01:03:46

Mike Volpi

Netscape had started. They released the Netscape navigator, which was the browser in, I want to say, february of 94.

01:03:56

Logan Bartlett

Okay, right around, right at the time. And you think this is the big thing. This is what you want to be a part of and you apply to Netscape. And Mark and Ben say, no, thank you.

01:04:09

Mike Volpi

Ben was not that senior yet, but Mark, yeah, no, what actually happened was I was an engineer. I was a mechanical engineer at Hewlett Packard before business school. When I got into business school, I had all these smart bankers and consultants. So like, oh, that's the way to go. So I got a job in management consulting over the summer. Didn't like it at all. I was like, no, I'm going back to tech. And I was organizing a conference and a friend of mine, Greg Sands, who's actually got his own venture firm now, was like, hey, rather than doing all these posters, I think we should make this thing called a website. And I was, a website. He goes like, yeah, there's this thing called a web browser and you can go check out the Louvre and all these things.

01:04:59

Mike Volpi

And we should make one of those. And we'll advertise the conference there. And we had emails, so we'll just get people's emails and that'll be, we'll make a little Excel spreadsheet. Like, okay, well, how hard is this making a website thing and so little HTML and whipped up a website, and then the conference was completely oversubscribed and people from all over the world showed up for this conference. And I was like, hallelujah. Wow, this thing is like, this web thing is super cool. And so my friend sans had a job offer to go to Netscape. He was like, ahead of me in terms of figuring it out. So I called sans and I'm like, yeah, do you think there might be one more job there? And he actually talked to the guys, like, now look, MBA with a mechanical engineering degree. You're utterly useless.

01:05:44

Mike Volpi

No, thank you. So then that's when I sort of took a step back and said, okay, well, how is an Internet made? And what are the pieces in there? And I figured out that the Internet is made out of routers, and there's one company that makes all the routers. And so I cold called the CEO of Cisco, who happened to be a Stanford grad also, and he was again, kind enough to open his door to me, and that led to a job.

01:06:08

Logan Bartlett

Who was the CEO of Cisco?

01:06:10

Mike Volpi

A guy named John Mortgage. He's the predecessor to John Chambers, who was largely my boss during my tenure at Cisco, but mortgage was the CEO. He's sort of this man from Wisconsin who now lives in New Hampshire, is kind of a know, simple man, but amazing mentor for me when I was young. And yeah, he found me interesting enough to give me a job.

01:06:35

Logan Bartlett

So you were there for a while and basically ran M and a bought, I think, over 100 companies, invested in 250 plus. Is there something that you learned about M and a that would be broadly applicable to an entrepreneur to be thinking about, even if everyone's aspirations are to go public and build a $20 billion company? But that's a logical landing spot for the vast, vast majority of companies. Is there anything that you experienced or saw that is worth imparting to an entrepreneur listening?

01:07:11

Mike Volpi

I would say that M A is something that makes sense at times. In particular, when you are at a distribution disadvantage to an incumbent and in roughly the same field, it's something that's worthy of thinking about because the incumbent tends to have a lot of staying power and will fight you for long periods of time, especially if they're large companies. So in the case of Cisco, if you were making a moderately competitive product, you could sell the company, hopefully get a reasonably good position in the company and sort of continue to grow with it, and at the same time not have to fight the fight forever. Now, not every entrepreneur faces that situation. Not everybody's got like a giant incumbent that they have to deal with. So it's case by case.

01:08:07

Mike Volpi

The other thing would be if you're going to sell your company, sell it to someplace where you're excited to go. Thankfully, at the time, Cisco was growing by leaps and bounds, growing 200% year on year. And if you get to join that and ride the wave, absolutely. A lot of times I think entrepreneurs just kind of think of it as, I'm done, I'm just selling out. I'm going to go there, waste my time for two years, and then go away again. And in truth, I think if I were an entrepreneur, I wouldn't not necessarily try to maximize value of how much money am I getting from Na, but am I going to the right kind of company where I'll actually not waste two years of my life vesting, but I'll actually do something productive and meaningful.

01:08:51

Mike Volpi

And you've sort of seen know when Facebook bought Instagram, Kevin Cisram was there for a long time. He didn't just sort of say like, oh, great, that was a billion dollars, thank you very much. Goodbye. He became an integral part of the company, and I think he enjoyed his ride at Facebook just much before afterwards. And I think that he probably could have sold Instagram to somebody else for more money. But I think in the end, both financially and personally, that became a much more fruitful endeavor.

01:09:20

Logan Bartlett

Yeah. Is there something that companies do or should do to set m a up for success on the acquirer side that you've kind of seen play out or that you would recommend?

01:09:35

Mike Volpi

When I was at Cisco, just during the period that I managed that part of the organization, I think we bought 75 companies in, as was the case as a VC, made every mistake in the book, like screwed all of them up, but some of them turned out to be meaningful. I think the most important thing that I've often talked about is that companies are not made to be bought and companies are not created to be acquirers. It's a very unnatural process. And when you do unnatural things as an organization or as a person, you tend to make a lot of mistakes when you do those. And so if acquisitions are going to be a core part of your strategy, make sure that you have processes built around it.

01:10:17

Mike Volpi

You hire people that know what they're doing around it, that you think of the end to end process of both evaluating, acquiring, integrating, and then measuring the success of that. Accept the fact that you're going to make mistakes. Just like for us vcs, you're going to make mistakes, but the good ones really work out. And the bad ones turn to zero. So understand that you can't just buy one and hope it's going to work, but you have to build business processes around it. And in the end, in all think, you know, Cisco probably won't necessarily say this in their public media, but my guess is their success rate on acquisitions was probably comparable to what we would expect as a success rate as vcs. They're sort of doing VC at a slightly larger scale.

01:11:01

Mike Volpi

But imagine being a VC and only doing one deal a year or one deal every two years. Would you get good at it? Not really. You just got to do it more. And most companies that acquire don't think of it that way. They're just like, oh, we found this very strategic thing, we'll do it one off. Well, chances are you're probably not going to get good at it doing that.

01:11:19

Logan Bartlett

You were a CEO for two years?

01:11:21

Mike Volpi

Yeah.

01:11:21

Logan Bartlett

Juice, was there anything, I'm sure there's things you wished you did differently, but did you, in retrospect, wish you had gone and been a CEO or founder earlier in the journey, or was that the right time for you to try it out?

01:11:38

Mike Volpi

Okay, so I should have done it sooner. Yeah. It was hard for me to leave Cisco because it was home. I'd grown up as a person in that process. Some of the people that I worked with there, Jay Sri Lal, Tony Bates, Charlie Giancarlo, these are people that are still my close friends. I became a person during that period of time. So it's very hard for me to go like, okay, I'm out of here. Probably men's ice overstayed my welcome there. And also, I think in the latter years, from about 2001 until 2007, when I left, the company was relatively static at 50, 60,000 employees. So you don't even notice. But your mindset becomes big company. Like, you start to think big company, and the values of what makes a big company good and a small company good are very different. Right?

01:12:40

Mike Volpi

And so I think when I became a CEO, the first mistake is that my mindset and things like velocity of decision making was very big company. And I didn't appreciate how much I needed to unwind the last five, six years of experience that I had to be a better leader of a small company. In big companies, there's a heavier cost when you change your mind on things. If I say, like, okay, I had like five, 6000 people working for me at Cisco, and I was like, okay, well, we're going to take like 500 of them and have them go do this you just blew up 500 people's lives in a startup. It's like, we're going to take three of you guys and you go do that, and it's like, tomorrow morning we wake up and it's like, oh, that was a bad decision.

01:13:27

Mike Volpi

Let's come back and do this. And that's like, no foul, no harm. It's a total two way door in decision making, whereas big company decision making is more of a one way door. It is reversible, but it's pretty painful. And so you become cautious, right? You do what I call you, play a little more defense than you play offense. And I think I stepped into the CEO role with too much defense in my mind and not enough offense in my mind. So that was probably a big, and I think had I done it earlier, when Cisco was still in its growth mode, I think my mindset would have been in a little different phase that was more aligned with what you needed to do in a small entrepreneurial company.

01:14:06

Logan Bartlett

Did that experience benefit you more as a board member, investor, or neither?

01:14:10

Mike Volpi

My startup, I juiced probably the best two years of learning I've ever had in life, honestly, more than my time at Cisco. I felt personal ownership of the decisions that were made and the weight of know things had gone so well for me, both personally and for the company at Cisco, that I felt a little bit invincible, maybe, and I got my ass kicked. So that was good, recognizing what one's good at. I worked with Ruloff and Danny Ruloff at Sequoia. Danny at index were my board members. Both were amazing. Learned a lot from them. And I admired and respected Danny so much that actually led me to deciding to join him as a partner at that point. So, yeah, I learned a lot about board members when the company is not executing at the way you want it to.

01:15:13

Mike Volpi

So, yeah, really great learning years. The company didn't really make much money. I think it was sold for some return to capital to the investors, but wasn't great. But still, for me, probably the two best years of learning.